- Flipkart Big Billion Days 2025: Unmissable Festive Deals Await

- Russian Cancer Vaccine. Is this vaccine 100% Effective?

- Sharma diverges from Congress line on West Asia, hails government’s diplomacy

- Supreme Court upholds harsher punishment for higher authority

- It's time to name and shame these Trump villains

Life insurance providers are well-prepared to navigate the GST exemption on premiums, effective September 22, 2025. Despite the loss of input tax credits, insurers are confident in mitigating impacts through strategic cost optimization and product repricing.

Life Insurance Industry Poised for Growth Despite GST Exemption Challenges

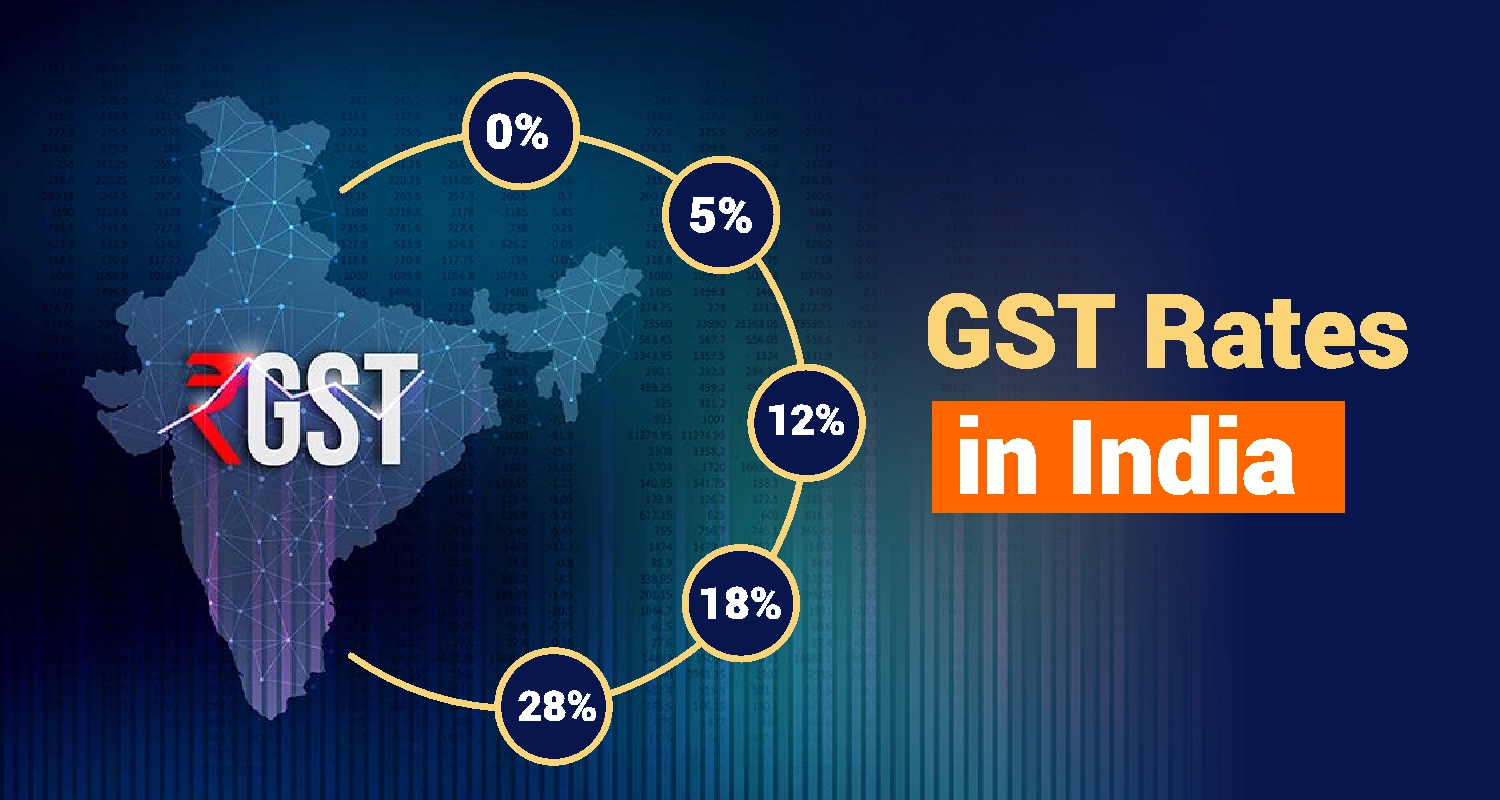

Starting September 22, 2025, life and health insurance premiums in India will be exempt from Goods and Services Tax (GST), a decision announced after the GST Council’s rate rationalization meeting. While this move aims to make insurance more affordable, it removes input tax credits (ITC) for insurers, prompting concerns about profitability. However, leading life insurance companies remain optimistic, leveraging strategic measures to minimize financial impacts and capitalize on long-term growth opportunities.

GST Exemption: A Double-Edged Sword

The GST exemption, as reported by sources like The Economic Times and Business Standard, is expected to lower premium costs for policyholders, potentially boosting insurance penetration in India. By eliminating the 18% GST on premiums, the government aims to make life and health insurance more accessible, especially for middle- and lower-income households. However, this comes at the cost of ITC, which insurers previously used to offset taxes on operational expenses like office costs, employee salaries, and marketing.

Insurers’ Confidence in Mitigating Impact

According to a Centrum Institutional Research report cited by The Economic Times, listed life insurance companies project a minimal impact on their Embedded Value (EV), with estimates suggesting a hit of less than 1%. Insurers are proactively addressing the ITC loss through strategies such as cost optimization, product repricing, and selective cost absorption. These measures aim to safeguard margins and maintain financial stability, as highlighted in analyses from Moneycontrol and Mint.

LIC’s Optimistic Outlook

The Life Insurance Corporation of India (LIC), the country’s largest insurer, has expressed strong confidence in navigating the GST changes. LIC anticipates an EV impact of under 0.5%, as per The Economic Times. The company views the exemption as a catalyst for industry growth, expecting an increase in the Value of New Business (VNB) as more customers opt for affordable policies. LIC’s robust market position and operational scale position it to absorb short-term challenges effectively.

Broader Industry Benefits

Industry experts, as quoted in Business Standard, suggest that the GST exemption could drive higher insurance adoption, particularly in underinsured segments. The affordability factor is likely to boost demand for term plans and health insurance, aligning with India’s goal of “Insurance for All” by 2047. Private insurers like HDFC Life and ICICI Prudential are also preparing to relaunch or reprice products to maintain competitiveness, according to Mint.

Short-Term Adjustments, Long-Term Gains

While the loss of ITC presents immediate challenges, the consensus among insurers and analysts is that the GST exemption is a net positive. The Centrum report maintains its sector outlook, emphasizing that strategic adjustments will limit financial strain. As insurance becomes more affordable, the industry anticipates sustained growth, with increased policy sales offsetting short-term margin pressures.

What’s Next for Policyholders and Insurers?

For consumers, the GST exemption translates to lower premium costs, making life and health insurance more attractive. For insurers, the focus remains on innovation and efficiency to navigate the ITC challenge. With proactive strategies and a favorable long-term outlook, the life insurance sector is well-positioned to thrive. Stay updated with trusted sources for the latest insights on India’s evolving insurance landscape.

Happy Streets returns to Bhartiya City in Bengaluru

Happy Streets, Bengaluru's beloved community event promoting car-free zones and active lifestyles, makes a vibrant return to Bhartiya City, drawing cr

Charter operators seek fair play in fuel pricing

Charter operators are pushing for equitable fuel pricing reforms to counter rising costs and ensure a level playing field in the industry.

AIBEA writes to FM seeking probe into HDFC Bank matter after chairman's exit

The All India Bank Employees Association has urged Finance Minister Nirmala Sitharaman to investigate alleged irregularities at HDFC Bank following th

How ‘eco-dystopian’ novels from Asia and Africa are pushing boundaries

Eco-dystopian novels from Asia and Africa are challenging traditional narratives by blending environmental crises with cultural insights, gaining glob

Subscribe to our mailing list to get the new updates!

Subscribe our newsletter to stay updated